Laid Off: Immediate Action Steps. Financials

[responsivevoice_button voice=”UK English Female” buttontext=”Listen to Post”]

If you’ve been laid off due to COVID-19, you are not alone. Hundreds of thousands of people lost their jobs because of the economic crisis caused by the pandemic. This sucks! I feel bad for all the people who got laid off. I feel terrible for my co-workers and friends, all the bright people who got let go. I know exactly how they feel, as I’ve been laid off myself. I am not a victim and don’t plan to stay without income or rely on a government to buy me food. I am a young, smart and healthy man. I’ve been through a lot and certainly prepared for the times like this. As I pull myself out this hole, I want to help others. How? I’ll write. I will write about the actions I take, thoughts I have to live the trace behind me for other to follow… or not.

My friend, you just “got kicked in your balls” pretty hard. The head spins from Whys and Ifs. Future is uncertain, however, there are few things that I can tell you for a fact:

- Your life will change dramatically from now on. Things will never be the same.

- You will feel uncomfortable.

- You will have put the work to stand back up.

- You will need to step over your ego and ask for help.

Realize, that thousand of people are in the same boat as me and you. Realize that NOBODY, I repeat, NOBODY knows what to do. We all just got equalized. This is not the finish, this is a start. The second you got your last paycheck, the gun went off.

“Take a break, you’ve been working so hard for so long. You deserve some time off.”

They say

That’s an option… for someone else. Buds, we’re a different breed. This is not an option for us.

“You’re young, you’ve got a lot of time. Relax.”

They say

The first part of this statement is true – you are young, however, I disagree with the second piece. You have no time! There is no time to waste on goofing around, blaming the virus, your employer, and feeling sorry for yourself. Life is just too great to waste it on those things, the world is too big to sit still. Take action!

Easy to say, but what exactly do I do now? Where do I even start?

Sit down, let’s brainstorm. You are not alone and I will help you figure things out. I don’t have all the answers, but I know the direction. I will help you clear things up and bring more clarity into your head.

First things first:

Food and Shelter

You need something to eat and you need the place to live. It all costs money, therefore the first step for you is to run some numbers and make financial projections.

Financials.

How long will you last?

Your bank account is not the flowing steam anymore, it’s a pond. There is no income coming in, so the pond starts to dry out. If you don’t change anything financially, it will dry out completely, leaving you broke AF. It’s not even a question if, but when. Know the exact date.

- You have some savings, how much? Put together all the cash saved from different accounts. Know exactly how much you have on hand.

- What are your monthly expenses? Go to your bank account and pull all the charges for the past three months. How much did you spend a month on average? What were the top 3 expenses? Know the numbers.

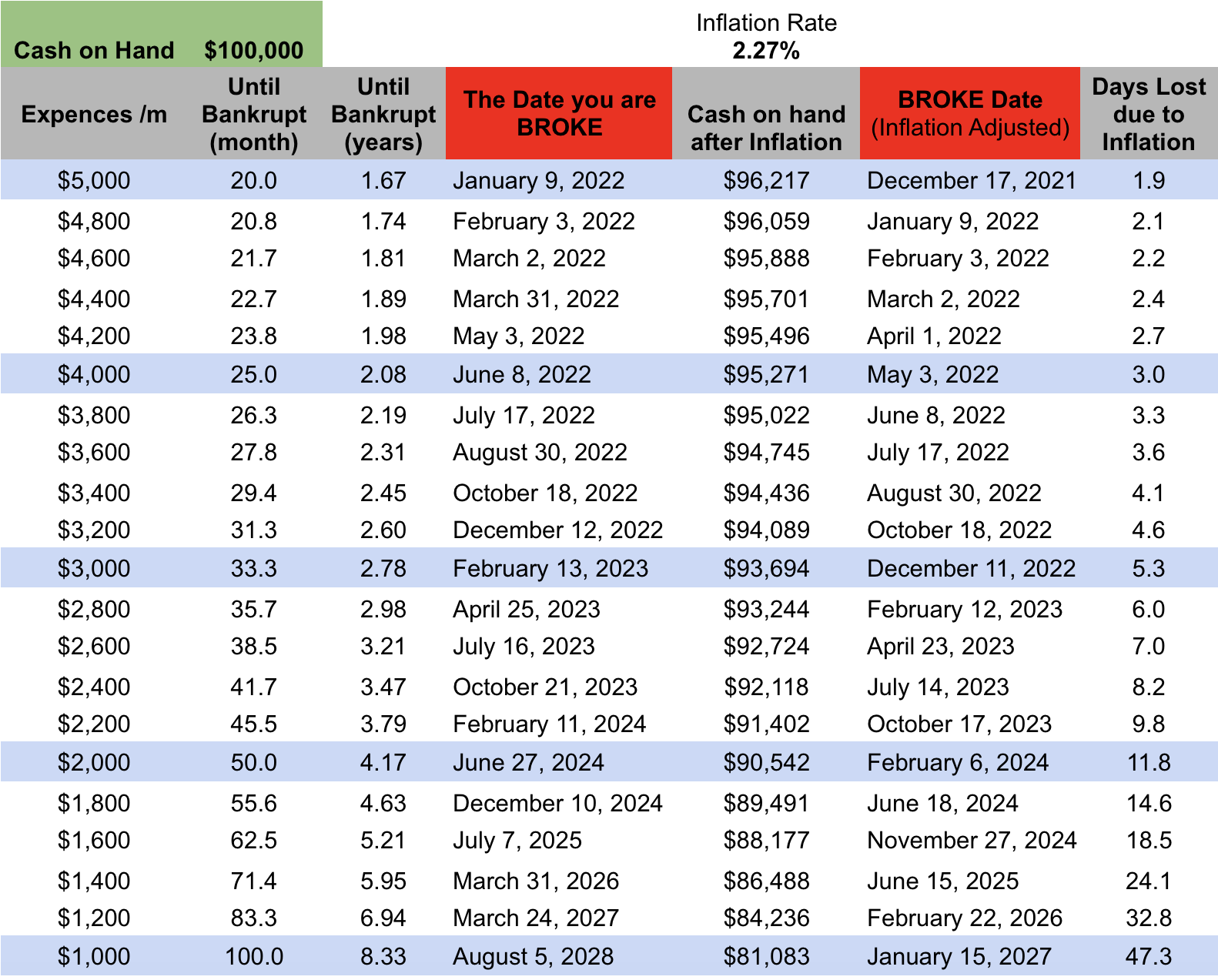

- Run financial forecasts. Experiment with different scenarios. See the example below for $100k saved. It shows how long you will last with this much income at different expense levels:

Calculations won’t be accurate without accounting for inflation. Not many people are aware of, however, this silent sucker takes the money out of your pocket at the rate of 2.27% (May 2020). Because money is not backed up by gold and the government prints it like crazy -> inflation will rise and your $100k will worth less as you go. The worst part is that this number is expected to rise over the next few years, moving the date of your bankruptcy closer at a higher speed.

At the current Inflation rate, your $100k will worth:

- 2 years -> $95k

- 3 years -> $93k

- 4 years -> $90k

- 6 years -> $86k

- 8 years -> about $80,000

Over the course of 8 years, you will lose at least $20,000 due to inflation. Of course, the number will fluctuate, however, don’t expect it to be much lower and prepare for the opposite.

Time is money, so how many months of living will the inflation shave off?

- 2 years -> ~3 month

- 3 years -> 6 month

- 4.2 years -> almost a YEAR!

- 8 years -> ~ 4 years…

As you can tell, the numbers grow exponentially…

Key Takeaways

- Know your numbers

- Play out different scenarios

- A dollar today > A Dollar tomorrow

- By holding onto your cash, you lose money daily

- You need to find a way to put this money to work, where they at least don’t lose in value over time

- If you don’t take action and change anything, your pond will dry out faster than you think. You will go broke

So what do you do now?

Immediate Action Steps

- Minimize your expenses. Cut down your expenses and stop spending your resources on anything you can’t eat and/or does not have direct implications on your health

- Stop unnecessary monthly subscriptions (Spotify, Netflix, etc.)

- Cancel all you travel and vacation plans (if you had any)

- Review your grocery bracket. Only necessities

- Do you REALLY need the car? Consider selling your vehicle. This will eliminate car insurance payments, gas, and amortization expenses. If you can’t live without one, get yourself something cheaper. The old beat-up sedan is an excellent choice.

- Lower your rent payments. Downside. If you are renting, this is probably one of the biggest expenses on your balance sheet. Can you move to a cheaper place? How can you minimize the monthly payments? No matter what you do, don’t move into the basement. I’ve got more on it here: 6 Months in Basement. It is not worth the savings! Lessons Learned.

2. Make a Long-Term Plan. Sit down with a pen and lots of paper. You need a plan! Three major questions you need to answer:

- How do I develop several streams of income?

- How can I get out of deflationary assets (cash)?

- How can I make a living with only the internet connection?

3. Execute Immediately. Stand up, wash your face, and get to work!