[responsivevoice_button voice=”UK English Female” buttontext=”Listen to Post”]

If you’ve been laid off due to COVID-19, you are not alone. Hundreds of thousands of people lost their jobs because of the economic crisis caused by the pandemic. This sucks! I feel bad for all the people who got laid off. I feel terrible for my co-workers and friends, all the bright people who got let go. I know exactly how they feel, as I’ve been laid off myself. I am not a victim and don’t plan to stay without income or rely on a government to buy me food. I am a young, smart and healthy man. I’ve been through a lot and certainly prepared for the times like this. As I pull myself out this hole, I want to help others. How? I’ll write. I will write about the actions I take, thoughts I have to live the trace behind me for other to follow… or not.

My friend, you just “got kicked in your balls” pretty hard. The head spins from Whys and Ifs. Future is uncertain, however, there are few things that I can tell you for a fact:

Your life will change dramatically from now on. Things will never be the same.

You will feel uncomfortable.

You will have put the work to stand back up.

You will need to step over your ego and ask for help.

Realize, that thousand of people are in the same boat as me and you. Realize that NOBODY, I repeat, NOBODY knows what to do. We all just got equalized. This is not the finish, this is a start. The second you got your last paycheck, the gun went off.

“Take a break, you’ve been working so hard for so long. You deserve some time off.”

They say

That’s an option… for someone else. Buds, we’re a different breed. This is not an option for us.

“You’re young, you’ve got a lot of time. Relax.”

They say

The first part of this statement is true – you are young, however, I disagree with the second piece. You have no time! There is no time to waste on goofing around, blaming the virus, your employer, and feeling sorry for yourself. Life is just too great to waste it on those things, the world is too big to sit still. Take action!

Easy to say, but what exactly do I do now? Where do I even start?

Sit down, let’s brainstorm. You are not alone and I will help you figure things out. I don’t have all the answers, but I know the direction. I will help you clear things up and bring more clarity into your head.

First things first: Food and Shelter

You need something to eat and you need the place to live. It all costs money, therefore the first step for you is to run some numbers and make financial projections.

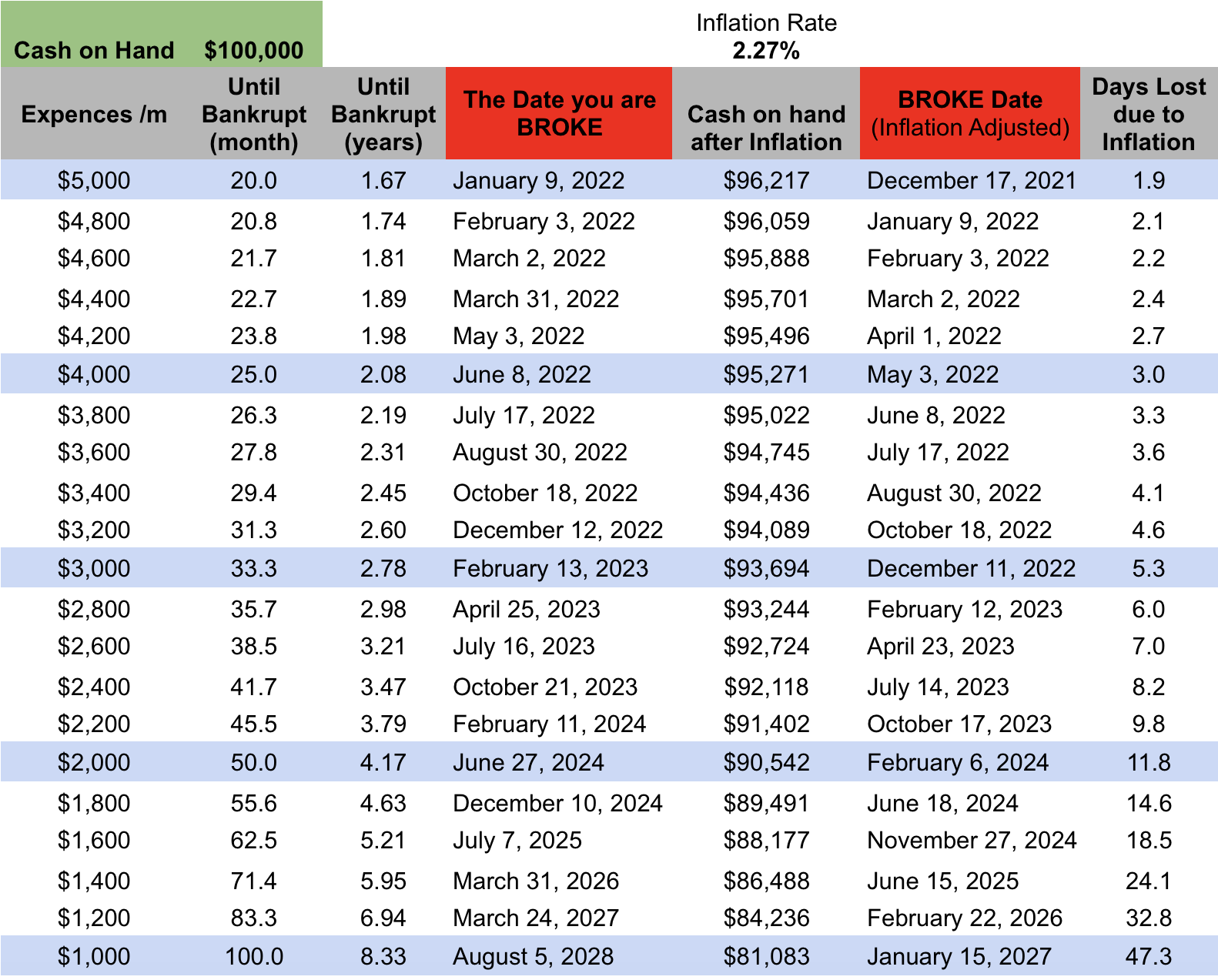

Financials. How long will you last?

Your bank account is not the flowing steam anymore, it’s a pond. There is no income coming in, so the pond starts to dry out. If you don’t change anything financially, it will dry out completely, leaving you broke AF. It’s not even a question if, but when. Know the exact date.

You have some savings, how much? Put together all the cash saved from different accounts. Know exactly how much you have on hand.

What are your monthly expenses? Go to your bank account and pull all the charges for the past three months. How much did you spend a month on average? What were the top 3 expenses? Know the numbers.

Run financial forecasts. Experiment with different scenarios. See the example below for $100k saved. It shows how long you will last with this much income at different expense levels:

Calculations won’t be accurate without accounting for inflation. Not many people are aware of, however, this silent sucker takes the money out of your pocket at the rate of 2.27% (May 2020). Because money is not backed up by gold and the government prints it like crazy -> inflation will rise and your $100k will worth less as you go. The worst part is that this number is expected to rise over the next few years, moving the date of your bankruptcy closer at a higher speed.

At the current Inflation rate, your $100k will worth:

2 years -> $95k

3 years -> $93k

4 years -> $90k

6 years -> $86k

8 years -> about $80,000

Over the course of 8 years, you will lose at least $20,000 due to inflation. Of course, the number will fluctuate, however, don’t expect it to be much lower and prepare for the opposite.

Time is money, so how many months of living will the inflation shave off?

2 years -> ~3 month

3 years -> 6 month

4.2 years -> almost a YEAR!

8 years -> ~ 4 years…

As you can tell, the numbers grow exponentially…

Key Takeaways

Know your numbers

Play out different scenarios

A dollar today > A Dollar tomorrow

By holding onto your cash, you lose money daily

You need to find a way to put this money to work, where they at least don’t lose in value over time

If you don’t take action and change anything, your pond will dry out faster than you think. You will go broke

So what do you do now?

Immediate Action Steps

Minimize your expenses. Cut down your expenses and stop spending your resources on anything you can’t eat and/or does not have direct implications on your health

Cancel all you travel and vacation plans (if you had any)

Review your grocery bracket. Only necessities

Do you REALLY need the car? Consider selling your vehicle. This will eliminate car insurance payments, gas, and amortization expenses. If you can’t live without one, get yourself something cheaper. The old beat-up sedan is an excellent choice.

Lower your rent payments. Downside. If you are renting, this is probably one of the biggest expenses on your balance sheet. Can you move to a cheaper place? How can you minimize the monthly payments? No matter what you do, don’t move into the basement. I’ve got more on it here: 6 Months in Basement. It is not worth the savings! Lessons Learned.

2. Make a Long-Term Plan. Sit down with a pen and lots of paper. You need a plan! Three major questions you need to answer:

How do I develop several streams of income?

How can I get out of deflationary assets (cash)?

How can I make a living with only the internet connection?

3. Execute Immediately. Stand up, wash your face, and get to work!

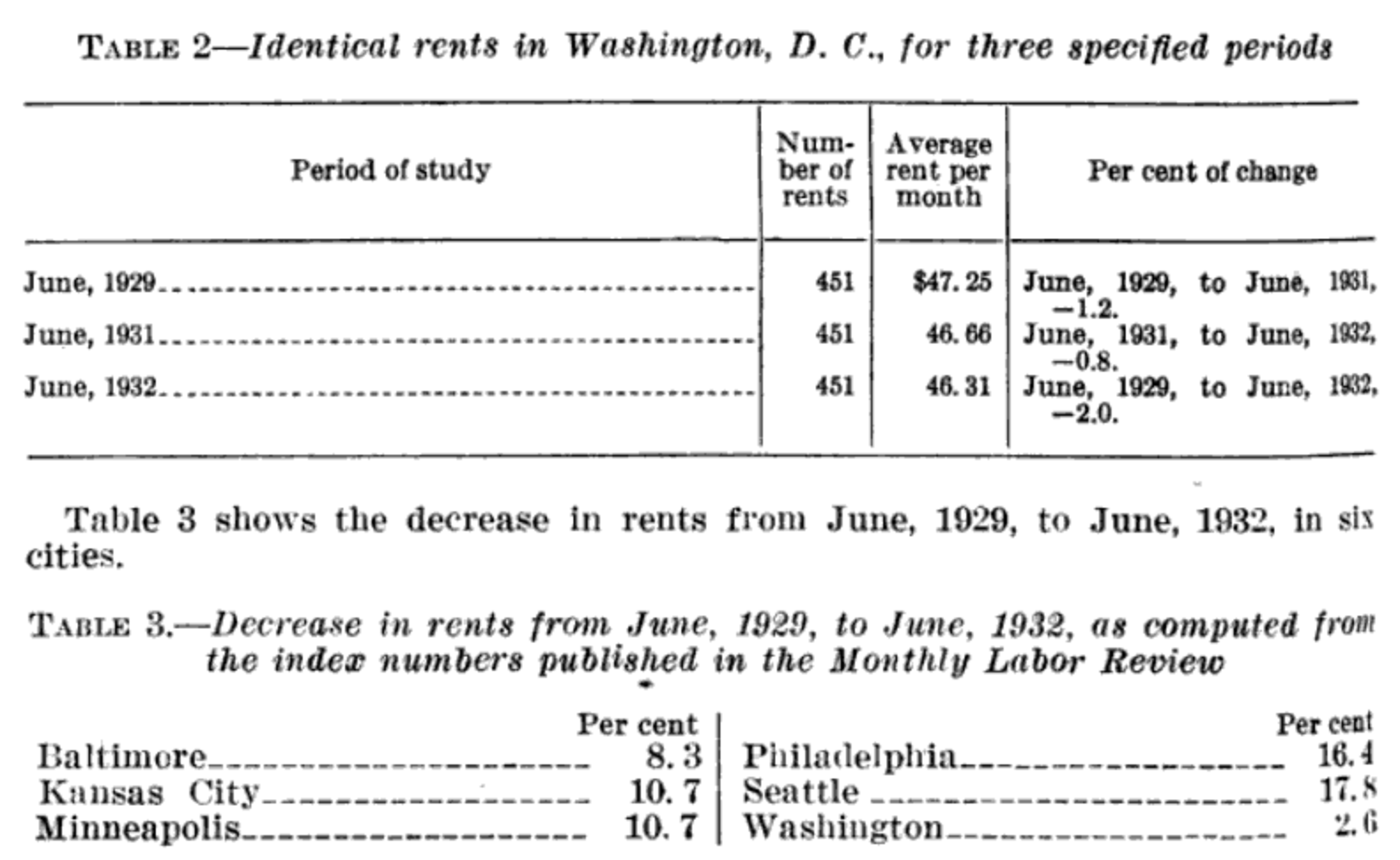

RENTS IN THE DISTRICT OF COLUMBIA The hearing of June 17, 1932, which appears below, was held prior to the approval by the Senate of Senate Resolution 248, directing an inquiry into the rental situation in the District of Columbia. The record of the following hearing is included herein, however, because of its close relationship to subsequent proceedings under the resolution.

FRIDAY, JUNE 17, 1932 UNITED STATEs SENATE, CoMMITTEE on THE DISTRICT of Columbia, Washington, D. C.

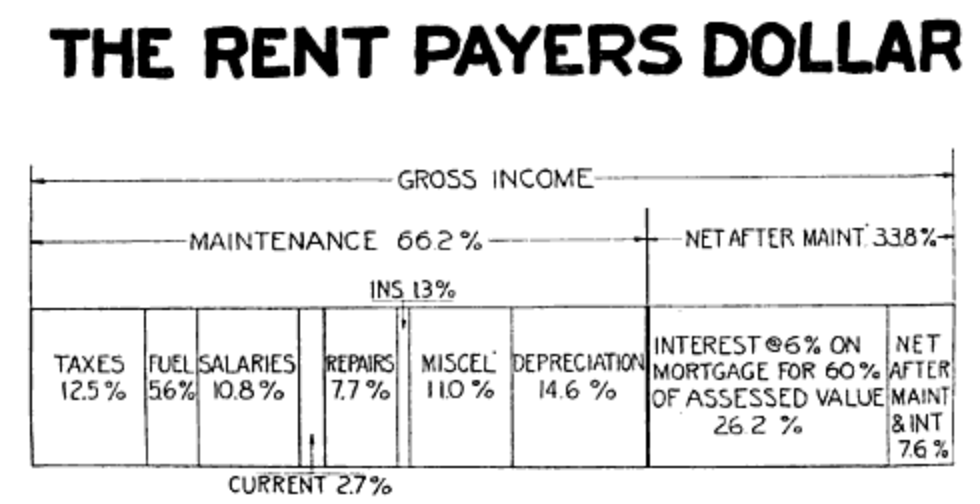

Mr. BRINKMAN. In a case where a building is mortgaged for $200,000 and the interest is 6 percent, if that interest rate were lowered to 5 percent and some of the excessive commissions charged for renewals every three years on these loans were eliminated, you would have a saving in interest charges and commissions of $2,500 on that loan. The usual rental of a building of that type is about $33,000. You could give the tenants of that building a 7 percent reduction in their rent, without diminishing the return to the owners at all, simply by lowering the interest rate 1 percent.

Mr. BowTE. Do you mean a building that you would loan $200,000 on would only produce $30,000 a year? Mr. WHITEFORD. That is the worst loan I ever heard tell of. Mr. BRINKMAN. $33,000. Mr. Bowie. Nine times. Mr. WHITEFORD. You talk about vicious loans. I am surprised at how little you know after all your study about this. Mr. BRINKMAN. Thank you for the insult.

The Rust firm took in the ‘Clifton Terrace Apartments at $750,000. The income from that property is sufficient to produce a net return of about 13 percent on the investment.

Apartment-House Game

Senator Copeland. Are you familiar with the apartment-house game at all? Mr. GoRDON. Fairly well. I know they are all broke. Senator Copeland. Well, is your business comparable to theirs? Are they better or worse off than you are? Mr. GoRDON. Well, I would say—I can not swear to this—more than half of the apartment houses in Washington have been foreclosed through the inability of the people to carry them. Either the Second or first trusts have been foreclosed and the people lost them. I think that is the best proof that they do not pay. Senator CAPPER. Well, were not the most of them financed for a great deal more than they had in them? Mr. GoRDON. Some of them, although a few firms here, which you probably know about, did some very wildcat financing, but we don’t account that. That was the exception. Most of our lenders here lend on an apartment house about 60 percent to 65 percent of the actual cash cost of the building and ground. That isn’t bad. Then, this man will have a second trust above that, maybe of 20 percent, and then when a smash comes, he gets squashed. Senator CAPPER. The second trust is where the high financing took place? Mr. GoRDON. Not necessarily. Senator Copeland. Your idea and contention is that even though there has been a foreclosure and new owners have taken possession, that with the amount of the investment they have to make, it goes up to the original cost? Mr. GoRDON. Well, maybe not that. He takes it over at $150,000. Maybe he will have to spend $15,000 to fix it up, but he may lose that much in vacancies before it is filled up again. Sometimes you have to take these houses and fumigate them with poison to get the bedbugs out. Senator KING. What do you allow for deterioration in buildings here per year? Mr. GoRDoN. Well, 2 percent or 3 percent. Senator KING. In 10 years a building costing $200,000 would deteriorate 20 percent? Mr. GoRDON. It may go further than that; and if the neighbourhood goes back, you get hit awful hard. It is a very risky business. Senator Copeland. Well, the present investment in an apartment house, according to your figures, is at least 25 percent less than the investment made by the original builder? Mr. GoRDON. I would say so, yes; but he hasn’t got a new building and is not getting the same rents, either. Keep your mind fixed on this: One-half of the apartment-house owners have lost their buildings because they would not pay. That is a fact. Look at the Star every evening and you will see big foreclosures all the time. Senator CAPPER. Do not the loan companies—the loan companies. are companies—the loan companies who are doing the financing—make the clean-up? They get the money.

House Values

Senator KING. Has there been a reduction in the value of the real estate in Washington during the past few years? Mr. GoRDoN. You can build houses now, the actual cost bein about 30 per cent less than you could four or five years ago. Ground has held its own. I am surprised it has, really. In many places vacant ground has gone up a little bit. Senator CAPPER. Are conditions in Washington in that respect better than probably any other city in the country? Mr. GoRDON, I consider Washington the safest city in the world. Senator CAPPER. Is it not due largely to the fact that there is a steady payroll here out of the Government Treasury? Mr. GoRDoN. Yes, sir. Senator Copeland. And no industrial life.

Construction and building new houses had become 30% cheaper. During the financial crisis, it is safer to live in non-industrial cities.

Land Value

Senator Copeland. And, as a matter of fact, the present value of the property is probably not half that? Mr. GoRdon. No; I would not say that. I would say the building is 30 percent off and the ground has held its own. I think that is it. The ground has held its own. Senator Copeland. Then, your judgment is that the average apartment house, thoroughly modern, is worth about 30 percent less? Mr. GoRDON. The building; yes. The ground at the same value. The ground has held up very nicely.

Buildings had lost about 30% in value!!! However, what is really interesting is that the land price remained the same… Investments in lad are much safer.

Senator Copeland. What about land values?

Mr. Do YLE. They are off in the majority of cases. There are instances where surrounding improvements naturally are holding or maintaining values, and in some places, they are going up, depending on the use of the particular property. Senator Copeland. Has there been anything abnormal in that? Mr. Do YLE. Just a general lack of demand caused by general conditions. Mr. BRINKMAN. If a building is worth given amount to-day, and if it would cost to reproduce that building 25 percent less than it cost to put it up originally, ought not rents to come down proportionately assuming the building was on a fair rental basis before? You would have a building worth less and you could not sell it on the market for the same price as when it was constructed. Should there not be a reduction of rentals? Mr. Doyle. There is no arbitrary situation where the landlord can dictate what he will get out of his property. He has to take what his tenant will pay. That is regulated by supply and demand. Mr. BRINKMAN. How much of a reduction should occur? Mr. Do YLE. It is not dependent on what costs have gone down, because we have in mind normal conditions and not abnormal conditions. Mr. BRINKMAN. You had a good many vacancies at 3901 Connecti cut Avenue, had you not? Mr. Do YLE. Yes. Mr. BRINKMAN. You reduced rents substantially, did you not? Mr. Doyle. They have been reduced. Mr. BRINKMAN. Did you rent a great many of the apartments? Mr. Do YLE. When we first took it over we did not reduce them as much. Vacancies occurred to some extent afterward. Rents were reduced in the last two months quite materially, and old tenants were given a month’s rent. Mr. BRINKMAN. And you were able to rent some of those empty apartments? Mr. Doy LE. It has been, through very careful and good management, rented up, and I think it is practically 100 percent rented. They are very reasonable rents, but it pays no return on its cost.

Construction Costs

Mr. BRINKMAN. How much have apartment building construction costs come down approximately in the last few years? Mr. Doyle. Approximately 25 percent. Mr. BRINKMAN. Twenty-five or 30 percent, would you say? Mr. Do YLE. I said 25. Of course, I am testifying.

The cost of construction reduced by 25%. It got much cheaper to build, hence it made sense to buy deteriorated houses just for the value of its land. Demolish -> Build a new house. However, if you wanted to build an apartment house and had to have a first-trust loan of $300,000 or $400,000, I do not think it would be humanly possible to get it. Build for cash?

Mr. WHITEFORD. I would not put a dollar in any building enterprise, and I do not think any other sagacious businessman would. Senator Copeland. I know you can now build property very much less than you could two or three years ago. I built a building three years ago and another this past summer. My cost on the second building was about one-third less than on the first one. There is not any question about that.

Rents

Mr. WHITEFORD. … we hear these complaints of distress that can not pay any rent. I know of people who are living in houses, in apartments, where they are not paying rent. They can not pay it. There are homeowners who can not keep homes. A man came in my office yesterday and asked me to loan him $200 to pay the little installment of interest due to his home, and it is a nice, great big home worth $20,000 odd. That man is suffering. He is in danger of losing his home for a few hundred dollars, but you can not do it by wishing you could. These property owners are in a jam. They are in difficulties and have their properties on valuations and purchase prices that go back for several years. Many of them are losing them now. Their security is jeopardized, for a lot of these properties are not worth the trust.

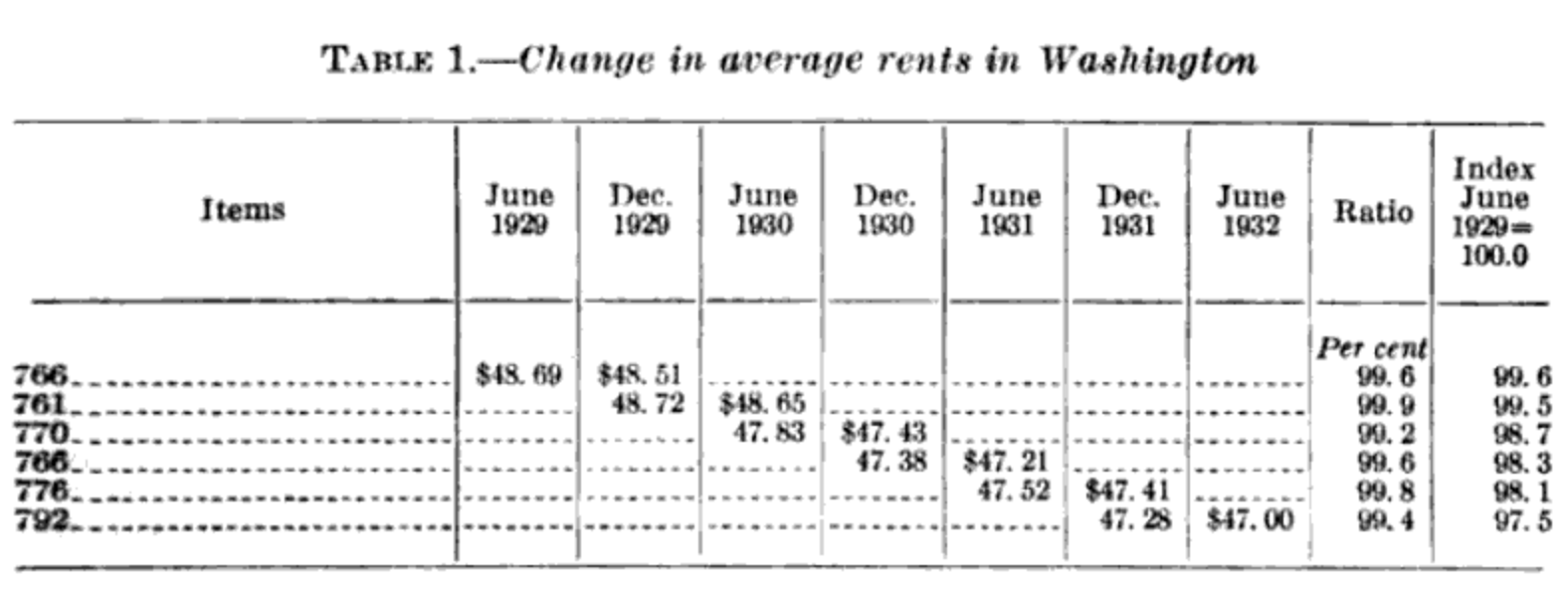

A drop of 2.5 percent in rents in Washington between June 1929 and June 1932.

The CHAIRMAN. In looking over Mr. Brinkman’s report I see that the reductions are very small. Mr. BRINKMAN. That is correct. Senator KING. You mean it is to the personal advantage of an owner to take charge of the rental of his own property? Mr. BRINKMAN. If I were the owner of the property I would not put it in the hands of a real estate agent, because I would have to pay them 5 percent commission, have to let him manage the property, buy supplies for it; pay in some cases 8 to 10 percent discount on purchases for the property, let them fix the scale of rates, and if a tenant is already a tenant of another member of the Real state Board, they will not accept him as a tenant. I will say it is a disadvantage in many respects for an owner of a property to turn it over to real-estate agents.

In order to reduce operational costs, owners will start managing properties on their own. Not the best time to be in the property management business.

Increase in rents by colored people

Mr. J. C. OLDEN. I represent the Better Citizens Bureau. I have made some further investigations with reference to the reduction of rent during the last week or so. I was to bring that further testimony to Mr. Brinkman, but they said they had closed reports on that matter. I can give the facts to this committee; as far as I have been able to find out in the apartment houses and houses that are rented by colored people there has been an increase in rents in the last three years and in some cases no reduction at all, possibly $2.50 or $3 reduction in an apartment. Senator Copeland. Does this cover a good many houses? Mr. OLDEN. Practically all the apartment houses rented by the colored in Washington. Senator KING. Are any of those apartment houses owned by colored people, to which you refer? Mr. OLDEN. No; they are owned by white people. Some have white agents and some have colored agents. Might not be the case in the modern world. I suspect there was much more racism back in the 30th. Mr. BRINKMAN. Properties are not worth the assessments? Mr. WHITEFord. Not to-day, they are not. Senator Copeland. I do not know any reason in the world why the landlords of Washington expect they are going to make money when nobody else in the world is doing it. Mr. WHITEFoRD. Most of them are not. Property owners and landlords, in particular, are losing money. If you had $500,000 you would not buy a piece of property and pay for it in cash. All large rental properties have trusts or mortgages on them made by an insurance company or trust company. There is no way in heavens world that they can escape paying 5 or 6 percent interest on their trusts and that interest rate was incurred several years ago. When you figure these properties have got to go on and pay that interest if they do not they will lose them.

Cash is King. Save cash, leverage.

Mr. WHITEFORd. The landlord gets to it every six months when he pays his interest. Sixty percent of the assessed value represents a fair mortgage, which is a fair way to approximate it. Senator Copeland… What percentage? Mr. WHITEFORD. Sixty percent of the assessed value. If that be true, then our figures show the property owner is getting less than 3 percent on his equity. Mr. WHITEFORD. Yes; and as Mr. Lusk says, it is less than savings bank interest; it is less than Liberty bond returns. Senator Copeland. Do you not think he would be lucky if he got enough to pay carrying charges? Mr. WHITEFORd. That is true. When you reduce the rent, you will have people that can not do it which will result in a series of foreclosures in the community.

Only sixty percent of the houses’ value is backed up by mortgage.

It seems to me that the owner and the agents overlook the great opportunity to increase the number of their tenants, and increase their income by reducing the rent.

Senator Copeland. I will tell you about my experience. I just came from Michigan where I went to see my father. My sister and I own some modest little homes and I asked her how she was getting along with the tenants. She said she cut the rent in two, in each instance, because by doing that she kept the tenant. They could not pay more than that, and if they had moved out because of the rental they had been paying, certainly she could not have rented the property to anybody else, because nobody else would pay it, but by making those reductions houses are occupied. As the chairman said, it seems to me in view of this great crisis, as it is going to be worse after this Congress adjourns, we have got to do something to take care of these people, and the landlords have just got to face the situation. If they do not cooperate they are go ing to lose anyhow, because these people can not the rent. They will have to reduce them or they will move out.

Mr. WHITEFord. We are reducing them. We have shown a lot of reductions, and experience shows it every day. Many of them are losing their property under foreclosure, anyhow, whether they reduce them or not. Senator KEAN. In the city of Elizabeth, where I come from, there is a row of apartment houses that used to rent for from $55 to $60 a month. They had been getting it right along, but now they are down to $27. Mr. WHITEFORD. If they have any trusts on the property they can not carry them.

Increase the number of their tenants, and increase their income by reducing the rent. How many tenants can you put under one roof? Now there are a lot of regulations that will restrict that.

Reference

United States. Congress. Senate. Committee on the District of Columbia. Subcommittee on Rental Investigation. (1932). Rents in D.C.: hearings before the United States Senate Committee on the District of Columbia, Subcommittee on Rental Investigation, Seventy-Second Congress, second session, on June 17, July 28, Sept. 9, Nov. 10, 30, Dec. 1, 2, 17, 20, 21, 23, 27, 29, 1932. Washington: U.S. G.P.O..

Below is my excerpt accompanied with main takeaways from the study published by Ray Dalio – an American billionaire hedge fund manager and economist, on April 23, 2020. (LinkedIn post)

We shouldn’t rely on governments to protect us financially.

We should expect most governments to abuse their privileged positions as the creators and users of money and credit.

All countries can print money to give to people to spend or to lend it out. However, not all money that governments print is of equal value.

You cannot create more wealth simply by printing more money and creating credit. To create more wealth, one has to be more productive. The relationship between the creation of money and credit and the creation of wealth (actual goods and services) is often confused yet it is the biggest driver of economic cycles.

Money and credit are stimulative when it’s given out and depressing when it has to be paid back. When the economy is growing too quickly and the government wants to slow it down, they make less money and credit available, causing both to become more expensive. When there is too little growth and central bankers want to stimulate the economy, they make money and credit cheap and plentiful, which encourages people to borrow and invest and/or spend.

The short-term cycles of ups and downs typically last about eight years. These short-term debt cycles add up to long-term debt cycles that typically last about 50 to 75 years. The last big long-term debt cycle, which is the one that we are now in, was designed in 1944 in Bretton Woods, New Hampshire, and was put in place in 1945 when World War II ended. However, these long-term debt cycles take about a lifetime to transpire, unlike the short-term debt cycles that we all experience a number of times in our lifetimes so most people understand better. When it comes to the long-term debt cycle most people, including most economists, don’t recognize or acknowledge its existence because, to see a number of them in order to understand the mechanics of how they work, one has to look at them operating in a number of countries over many hundreds of years in order to get a good sample size.

When it is widely perceived that the money and the debt assets that promise to receive money are not good storeholds of wealth, the long-term debt cycle is at its end, and a restructuring of the monetary system has to occur.

When countries were at war and there was no trust in the intentions or abilities to pay, they could still pay in gold. So gold (and to a lesser extent silver) could be used as both a safe medium of exchange and a safe storehold of wealth.

A person puts money in a Bank in exchange for interest (profit) -> Bank lends that person’s money to somebody else in exchange for a higher interest (profit) -> Those who borrow the money from the Bank like it because it gives them buying power that they didn’t have. Everyone is happy.

Trouble approaches when either there isn’t enough income to survive one’s debts or the amount of the claims (i.e., debt assets) that people are holding in the expectation that they can sell them to get money to buy goods and services increases faster than the number of goods and services by an amount that makes the conversion from that debt asset (e.g., that bond) implausible.

Think of debt as negative earnings and a negative asset that eats up earnings (because earnings have to go to pay it) and eat up other assets (because other assets have to be sold to get the money to pay the debt). When incomes and the values of one’s assets fall, there is a need to cut expenditures and sell off assets to raise the needed cash (to pay the debt).

When that’s not enough, the following happens:

Debt restructurings where debts and debt burdens are reduced, which is problematic for both the debtor and the creditor because one person’s debts are another’s assets

Central bank printing money and the central government handing out money and credit to fill in the holes in incomes and balance sheets (which is what is happening now). It occurs when holders of debt don’t believe that they are going to get adequate returns from it.

When people go to Banks and take the money they invested (for interest) out of it to buy goods and services, the bank has two choices:

Allow that flow of money out of the debt asset (raise interest rates and cause the debt and economic problems to worsen).

Print money.

An important difference between money and debt. Money is what settles claims—i.e., one pays one’s bills and one is done. Debt is a promise to deliver money.

This Already Happened Before… Several Times

In 1971, on the evening of August 15, when President Nixon spoke to the nation and told the world that the dollar would no longer be tied to gold. This led to stock prices rising. On Sunday evening March 5 President Franklin Roosevelt gave essentially the same speech doing essentially the same thing which yielded essentially the same result over the following months (a devaluation, a big stock market rally, and big gains in the gold price). That happened many times before in many countries, including essentially the same proclamations by the heads of state.

The coronavirus triggered economic and market downturns around the world, which created holes in incomes and balance sheets, especially for indebted entities that had incomes that suffered from the downturn.

When credit cycles reach their limit, the following events take place:

Interest Rates fall down. When there isn’t much room to stimulate by lowering interest rates (or printing money and buying financial assets) the greater the likelihood that there will be a monetary inflation accompanied by economic weakness. Stimulating money and credit growth by lowering interest rates is the first-choice monetary policy of central banks.

The government prints more money and creates additional debt. It is both the logical and the classic response for central governments and their central banks to create a lot of debt and print money that will be spent on goods, services, and investment assets to keep the economy moving. That is what was done during the 2008 debt crisis when interest rates could no longer be lowered because they had already hit 0%. As explained that was also done in response to the 1929-32 debt crisis when interest rates had been driven to 0%. This creating of the debt and money is now happening in amounts that are greater than at any time since World War II. The European Central Bank, the Bank of Japan, and—to a lesser extent—the People’s Bank of China made similar moves.

People will shift their wealth into other things. Current money printing increases the chances that money will be printed too aggressively and not used productively so people will stop using it as a storehold of wealth and. They also often move their wealth to other storeholds of wealth like gold, certain types of stocks, and/or somewhere else (like another country that is not having these problems).

People will seek to sell their debt assets and/or borrow money to get into debt that they can pay back with cheap money.

Such periods of reflation either stimulate another money and credit expansion that finances another economic expansion (which is good for stocks) or devalue money so that it produces monetary inflation (which is good for inflation-hedge assets such as gold).

Economic stress caused by large wealth and values gaps, will lead to higher taxes and fighting between the rich and the poor. The rich move to hard assets and other currencies and other countries. Those countries that are suffering from this flight from their debt, their currency, and their country will want to stop it. Expect governments to try to make it harder to invest in assets like gold (e.g., via outlawing gold transactions and ownership), foreign currencies (via eliminating the ability to transact in them), and foreign countries (via establishing foreign exchange controls to prevent the money from leaving the country).

When there is a large wealth gap, big debt problems, and an economic contraction, there is often fighting within countries and between countries over wealth and power. Also this will lead to domestic and international political changes.

The governments will go back to some form of hard currency (e.g., gold or a hard reserve currency) to rebuild people’s faith in the value of money as a storehold of wealth.

People will start selling their assets. To deal with that monetary inflation crisis and break the inflation, the supply of money will get tightened, which will drive interest rates to the highest level “since Jesus Christ”. Debtors will have to pay much more in debt service at the same time as their incomes and assets fall in value. This will squeeze the debtors and require them to sell assets.

We shouldn’t rely on governments to protect us financially.

We should expect most governments to abuse their privileged positions as the creators and users of money and credit.

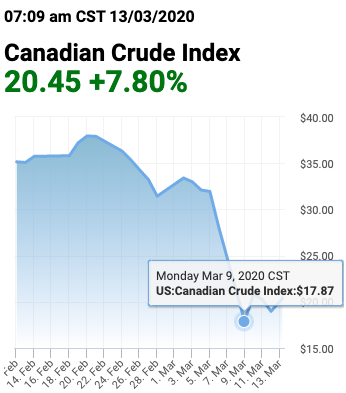

You have already noticed that the gas prices went down. Significantly! The first drop started on February 21st (Friday). Nothing critical, a slight fall down which had stopped on February 28th (Friday), exactly in a week. We are witnessing the Oil War – an epic battle between Russia and Saudi Arabia.

Why did the fall stop?

Why did it rise back up? Briefly, but it id

Did someone regulate it?

Was there events that caused the stall?

Is there an economic mechanism for oil price regulation?

Who controls the oil prices? OPEC or the Organization of the Petroleum Exporting Countries was formed to negotiate matters concerning oil prices and production.

How does OPEC do it? OPEC controls oil prices through its pricing-over-volume strategy. … Thus, when there is a glut of oil in the world, OPEC cuts back on its production quotas. When there is less oil, it increases oil prices to maintain stable levels of production.

Why do oil prices fall? Factories have been idled and thousands of flights canceled around the world as the coronavirus outbreak. People work from home – they drive less. Shrinking demand for jet fuel, gasoline and diesel. And now – the travel ban between the United States and Europe. It’s a nightmare scenario for the oil market.

What cheap oil means?

You will benefit from lower oil prices and the resulting decline in gas prices at the pump, especially in the United States where retail markets react more directly to supply and demand.

If you work on oil somewhere in the plant in Texas, Louisiana, Oklahoma, New Mexico or North Dakota, you will most likely lose your job.

People are being asked to isolate themselves. This is against human nature, therefore people will find other “safe” ways to socialize. Because people won’t socialize as much, they won’t buy a lot of jewelry and accessories. Apparel industry will also see a dip.